The CDP Institute—which researches the customer data platform (CDP) industry—has published its first State of the CDP Industry report for Europe, the Middle East and Africa (EMEA) in 2022, exploring how the industry is shifting from the early adopters to the mainstream market. The report, commissioned by Treasure Data, explores the strength of the industry; the EMEA market has increased notably with funding for vendors increasing from €210 million in 2020 to an estimated €496 million ($564 million) in 2022. And as EMEA business leaders and marketers navigate an increasingly difficult data landscape accelerated by COVID-19 and the pending loss of third-party cookies, the value of CDP services has never been more significant. The January 2022 industry update report can be downloaded from the CDP Institute website. A free CDP Institute membership is required to download the PDF report but below we’ve summarized the key highlights. For the full study, see Customer Data Platform Industry in EMEA.

From the Fringe to the Mainstream

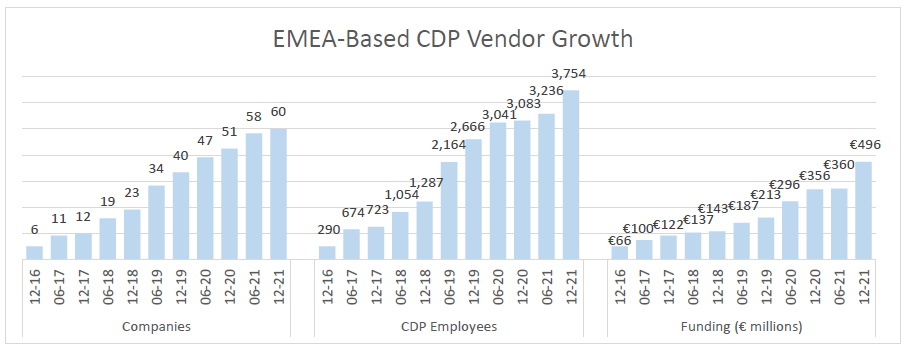

The CDP institute identified 60 vendors based in EMEA across 19 countries by the end of 2021, growing from 40 vendors in 2020.

Revenues for the region in 2021 were expected to be around US$ 570 million. In addition, another $230 million was expected by CDP vendors not based in EMEA.

EMEA vendors comprise 39% of companies, 27% of employees, and 28% of funding compared to the global market.

Interpreting First-Party Data is Utmost Priority

The pending loss of third-party cookies and the expansion of data privacy regulations is also driving interest in CDPs, as companies look for new ways to improve the capture of first-party data. The shift from third- to first-party data has prompted demand for the provision and unification of data ingestion via a scalable, manageable platform. Alongside this, due to strong GDPR restrictions prevalent in EMEA countries, there is increasing expectation among consumers for use of their data in an ethical and privacy-safe manner. The role of a CDP in these instances is evolving to one which helps support marketers through this transition, ensuring the privacy of consumers is adequately safeguarded. Ultimately, CDPs are offering businesses guidance and navigation through what is an evolving and increasingly complex regulatory landscape, facilitating the necessary shift from product-centric to customer-centric business across EMEA.

CDP Literacy Preventing Widespread Adoption

The benefits of a CDP still require communicating to unlock further growth and interest. Awareness about the difference between CDPs and non-CDPs, for example, is crucial for marketers to start making better choices, enabling them to identify a CDP that best meets their needs. In some cases, non-CDP vendors such as those in marketing automation, BI or CRM solutions even suggest that their solution can provide all the functionality of a CDP. When it comes to implementing these platforms post-purchase, marketers are then confronted with missing functionality and additional work to create the solution desired. In this expanding marketplace where customer data-driven marketing is high but maturity is still relatively low, confusion can be reduced by effectively explaining the differences between CDPs and non-CDP solutions to help marketers properly select and optimize a data solution for their businesses. Today’s CDP institute report reiterates the critical role of data-driven marketing strategies for business success as marketers wake up to the benefits of a CDP solution in an increasingly online and regulated landscape. As the CDP industry continues to grow, marketers are increasingly aware that to optimize their customer data, a CDP solution is integral to making it a success.

Related Articles

- CDP Industry in EMEA — Analyst research on CDP market expansion in Europe

- CDP Industry Market Trends 2023 — Budget tightening and new CDP value propositions in 2023